Tax Briefing, Summer 2023

This issue will cover;

- Settle the tax with a PSA

- Excess mileage payments

- Getting ready to retire

- What state pension will you receive

- VAT on work in pharmacies

- VAT on land and buildings

- Student loans, property and pensions

- Sales till manipulation

- Avoid payroll problems with duplicated employees

Settle the tax with a PSA

Occasionally you may reward your employees with something special such as a holiday or a hamper. If the value exceeds the tax-free amount permitted under the rules for say long service awards, trivial benefits or staff suggestions it will be taxable.

To avoid your employees getting a nasty shock in their pay packet you can bear the tax and NIC on their behalf under a payroll settlement agreement (PSA) negotiated with HMRC. The PSA procedure can also be used where the value of certain benefits provided to a group of employees such as taxis home after working late or a staff party exceeds the exempt amount.

Before entering into a PSA be aware that the costs can be significant as the tax and NIC due on the benefit must be grossed up. For an additional rate taxpayer the tax and NIC can amount to 115% of the value of the benefit provided. However this cost should be weighed against the savings in administrative time and employee goodwill.

Until recently the PSA had to be applied for using the paper form P626 but this can now be done online. Whether you use the paper form or the online facility HMRC will send the finalised agreement by post, although a confirmation or receipt of your application will be sent by email or letter.

To set up a PSA for occasional benefits provided in 2022-23 you must enter into the agreement with HMRC no later than 5 July 2023. The tax and NIC due under that PSA must be paid by 22 October 2023.

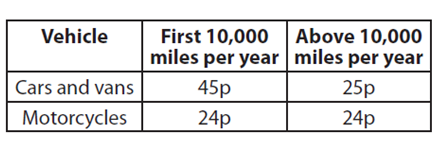

Excess mileage payments

Petrol and diesel pump prices are high but the tax-free mileage rates payable to employees who use their own vehicles for business have not been adjusted for over a decade.

Many employees cannot afford to use their own car or motorbike for business journeys if they only get reimbursed at these rates (see table) so some employers choose to pay more. But any excess above the tax-free rate is taxable and subject to NIC.

The guidance from HMRC is confusing but the simplest way to deal with the excess mileage payments is to treat them as extra salary and put them through the payroll. This treatment should be communicated to the affected employees.

Where the employee’s car is purely electric the employer can still pay up to the rates in the table tax and NIC-free. Where the employee charges their private electric car at a charging point at work for free there is no taxable benefit on the electricity.

Things get more complicated if the employer pays for the employee to charge their private electric car at the employee’s home or a roadside charging point.

Getting ready to retire

The changes to the pension rules announced in the Spring Budget were designed to dissuade higher earners from retiring early to avoid pension charges on high contributions but the new rules could have the opposite effect.

Individuals can now contribute up to £60,000 per year into a pension scheme and any excess allowance can be carried forward for up to three years.

Older taxpayers with substantial pension pots worried that they would be taxed at 55% when they started to draw their pension but this penalty rate has been removed. You can now build up any amount of savings in your pension fund.

It is also easier to carry on making pension contributions once you have started to access your pension benefits as the money purchase annual allowance (MPAA) has been increased to £10,000. You can thus take an annuity from one pension pot and continue to pay up to £10,000 per year into another scheme. Seek independent financial advice before deciding how or when to take your pension benefits.

If you run your own company you should consider the tax relief the employing company receives for any contribution it makes into your pension plan. The tax deduction is only given for the accounting period in which the contribution is actually paid – the cost cannot be accrued or pre-paid.

As the corporation tax rate is now 25% for companies with profits above £250,000 and a marginal rate of 26.5% applies on profits between £50,000 and £250,000, pension contributions can be used to bring corporate profits down to the desired profit level. We can help you work out the numbers specific to your business.

What state pension will you receive

The amount of your state pension is largely determined by how many years of NIC you have completed during your working life. You can check your NIC record in your online personal tax account (www.gov.uk/personal-tax-account).

You normally need 35 full years of NIC to receive the maximum state pension and ten complete years to receive any state pension. If you are under 45 you have plenty of time before you reach the state retirement age of 67 (or possibly 68) to make up for any gap years in your NIC record.

If you are 45 or older you have less time to pay NIC in the regular way on your wages or as a self-employed trader. The Government is currently encouraging women born after 5 April 1953 and men born after 5 April 1951 to make up any deficiency in their NIC record.

If you fall into this group you can pay voluntary NIC at £15.85 for each missing week in any tax year back to 2006-07 but this payment must be made by 31 July 2023. Payments after that date can only be used to fill NIC gaps in the years 2017-18 to 2022-23 and must be paid at the higher rate of £17.45 per week.

Paying voluntary NIC is effectively an investment decision. Consider whether paying extra NIC now will pay back sufficiently in the form of extra state pension over your expected lifetime.

VAT on work in pharmacies

For a medical service to be exempt from VAT it must generally be performed by a registered health professional or a staff member who is directly supervised by a registered health professional. Pharmacists can also deliver VAT exempt medical services but until recently that exemption did not apply to services delivered by pharmacists’ staff.

To ease the pressure on GP surgeries patients are encouraged to contact their community pharmacy for basic health advice. From 1 May 2023 medical services can be exempt if they are performed by a person who is not a registered health professional but who is directly supervised by a pharmacist.

This change will affect around 14,000 community pharmacies across the country and will mean that some of those businesses may become partially exempt for VAT.

VAT on land and buildings

When purchasing commercial premises you need to know whether VAT will be added to the price as the stamp duty land tax charge (or similar taxes in Wales or Scotland) is calculated on the VAT inclusive value.

Most older commercial buildings will be exempt from VAT but not if the owner has opted to apply VAT and informed HMRC. The option to tax (OTT) applies for up to 20 years so it is important to confirm the correct VAT position.

HMRC will no longer confirm whether VAT should be added to the price if the OTT decision was made less than six years ago. Questions regarding an OTT decision recorded over six years ago will be actioned by HMRC but not with any urgency.

If the building owner has gone into receivership HMRC will respond to requests regarding OTT decisions from insolvency practitioners appointed to administer the property in question.

Where an OTT decision is made and submitted to HMRC by email it will be acknowledged automatically but no further confirmation will be sent. The building owner is responsible for recording and preserving the OTT decision should HMRC ever ask, or a potential purchaser need proof of the VAT status of the building.

Student loans, property and pensions

Student loan repayments (SLR) are normally deducted under PAYE from employment income so many people incorrectly assume that SLR are not due on other ‘unearned’ income such as rent or pensions.

SLR will in fact be payable where the unearned income exceeds £2,000 per year and the taxpayer is required to submit a tax return.

Unearned income includes:

• interest from savings (before deduction of the personal savings allowance);

• profits from letting (after deduction of property allowance); and

• pension income

Once the unearned income exceeds £2,000 the whole amount is subject to SLR deducted at 9%.

Eve’s property

Eve earns £21,000 per year and has a plan 1 student loan for which the SLR threshold is £22,015 for 2023-24 so she is not liable to pay SLR on her earnings.

However Eve lets a property for £12,000 per year and after deducting expenses makes a profit of £3,000. Eve must include these figures on her tax return and pay SLR at 9% on rental profits of £1,985 (21,000 + 3,000 – 22,015) as the total property income profits exceed £2,000.

Adam’s pension

Adam is aged 60, earns £27,000 and has a plan 2 student loan for a teaching course undertaken as a mature student. The repayment threshold for plan 2 loans is £27,295 for 2023-24 so Adam is not liable to pay SLR on his earnings.

Adam has also started to draw a pension of £4,000 per year which is taxed under PAYE but is not subject to the SLR at source as no Class 1 NIC is due on that pension income.

However Adam has sundry trading income of £2,500 from selling free-range eggs from his hens. As this exceeds the trading allowance of £1,000 Adam must submit a tax return to report that trading income.

Adam’s additional income reported on his tax returned is £6,500 (£2,500 + £4,000) and he will have to pay SLR at 9% on £6,205 (27,000 + 6,500 – 27,295).

Sales till manipulation

The traditional way to hide sales from HMRC is to take payment in cash and not put it through the books.

Nowadays technology helps dishonest traders to hide sales by using electronic sales suppression (ESS) software. The sale is not recorded on the normal till record and the payment may also be diverted to a non-business bank account by manipulating the card-reader.

Last year HMRC raided 90 businesses involved in designing and marketing ESS software and as a result has a list of the names and addresses of businesses who bought that software. Users of ESS software may receive a letter from HMRC inviting a full disclosure of any undeclared sales and tax which should have been paid thereon.

Users will have 30 days to make the disclosure using the special online process for ESS declarations so there is not much time to mull-over what to do. If you receive a letter but have not deliberately hidden any of your sales you need to respond quickly to HMRC. If you do not respond within 30 days HMRC will either open a tax enquiry into your business or issue assessments for estimated amounts of unpaid tax.

Interest will be due on any late paid tax plus penalties for:

• late payment of tax;

• inaccurate VAT, corporation tax or income tax returns;

• failure to register for VAT, corporation tax or income tax; and

• possession of ESS software

Traders who have used ESS software are in serious trouble as HMRC view this as tax fraud which is a criminal offence, although in most cases HMRC will agree a civil settlement.

Ask us for advice if you receive a letter from HMRC about ESS.

Avoid payroll problems with duplicated employees

When HMRC asks for more PAYE than you have deducted from your staff’s wages it is often the result of double-counting somewhere in the process.

A persistent bug in the PAYE system is caused by the HMRC computer creating a duplicate employment record which it then uses to demand PAYE for wages which have not been paid.

For example William Smith earns a regular salary of £2,000 per month. On the first payroll return he is correctly recorded as William Smith. However on a later return his name is abbreviated to Bill Smith. The HMRC computer will assume that William Smith and Bill Smith are two different people.

As the employment record for William Smith has not been closed the computer will generate a PAYE charge on the basis that you have paid £4,000 in total that month to William and his doppelganger Bill.

To avoid HMRC creating duplicate employment records:

• use consistent employee names;

• use a unique payroll number for each employee;

• do not re-use employee payroll numbers;

• where an individual re-joins your payroll after leaving, give that person a new payroll number and reset their year-to-date payment information to zero;

• only include the start date on the first FPS when a new employee joins – do not alter that start date later;

• use the ‘irregular payment pattern’ indicator for any employee who is paid infrequently

Be particularly careful with payroll numbers. If you are using new payroll software for the first time or are merging two payrolls, meaning new payroll numbers are needed, use the payroll ID ‘change indicator’ box in your PAYE return. We can help you with this.

If you receive a demand for additional PAYE please contact us without delay.

Get in Touch

Please contact us if you need further advice, have any questions about our services, or would like a free consultation or a fixed quote.