Tax Briefing, Autumn Budget 2022

This issue will cover;

- Income tax cuts next year

- Share schemes explained

- IR35: Contractors delighted by changes

- Companies spared tax rise

- Home buyers to pay less stamp duty

- Crack down on cloned companies

- Tax incentives in investment zones

- NIC cut in November

Income tax cuts next year

In last week’s Budget the Chancellor stunned his audience by announcing that both the basic rate of tax and the highest ‘additional’ rate would be reduced from 6 April 2023.

Around 50% of taxpayers only pay tax at the basic rate and they will benefit from that rate being reduced from 20% to 19%. This had been announced by the previous Chancellor but was not going to be introduced until 2024. Moving this a year earlier has been done, we are told, to help with the cost of living crisis.

The income threshold at which taxpayers start to pay tax at 40% and the personal allowance have both been frozen for five years from April 2021 to April 2026. With inflation running at nearly 10% this will reduce the real value of the tax-free personal allowance and drag more people into the higher rate tax bracket.

Higher earning individuals will benefit the most from the Budget as the 45% additional rate of tax that applies on income over £150,000 will be abolished from 6 April 2023. These taxpayers will also be eligible to benefit from the £500 savings allowance for the first time from April 2023. The 40% rate will simply continue to apply to all higher levels of income.

These tax cuts do not apply in Scotland as the Scottish Government sets its own income tax rates on earnings and profits (not savings and dividends) which currently range from 19% to 46%. This may change when the Scottish Budget for 2023-24 is announced later this year. The Welsh Government will also have to decide whether to follow Westminster and apply tax cuts to match those in England from 2023.

In addition to cutting tax on earnings the Chancellor has chosen to cut the tax payable on dividend income by 1.25 percentage points from 6 April 2023. This cut will apply across the whole of the UK.

From 6 April 2023 the rates of income tax in England and Northern Ireland will be:

Share schemes explained

Several investment schemes provide a basket of tax reliefs to individuals who are prepared to risk their money by subscribing for new shares in small trading companies.

Two such schemes are the Enterprise Investment Scheme (EIS) and the similar Seed Enterprise Investment Scheme (SEIS) for early stage trading companies. These schemes were due to end in 2025 but they will now be extended for an indefinite period. The amount that each investor can invest under the SEIS will be doubled to £200,000 per year from 6 April 2023.

The conditions for a company using the SEIS to raise funds will also be relaxed so that it can raise up to £250,000 and have assets of up to £300,000. Currently such companies must be within two years of starting their trade when they receive funds under the SEIS and this will be extended to three years. Employers can encourage their employees to take a stake in the company by providing them with share options. Under the Company Share Option Plan (CSOP) employees can be granted share options with a market value of up to £30,000 and the Chancellor has proposed doubling this cap to £60,000 from April 2023. If you are looking to raise money to start or develop a business, or simply to motivate and retain staff, we can advise you on the best schemes for your needs.

IR35: Contractors delighted by changes

The Chancellor has said that he will abolish the hugely complicated off-payroll working rules from 6 April 2023.

These rules require large businesses and public sector bodies to decide whether the contractors that they engage act as employees (in tax terms) and should be taxed as such under the IR35 rules. Any agencies or intermediaries in the hiring chain are ignored for this decision.

To be clear the underlying IR35 rules are not being abolished. The only change from 6 April 2023 is that the responsibility for deciding whether the IR35 rules apply to a particular contract will revert to the contractors and consultants who provide their services through an intermediary such as their own personal service company.

The risk of getting the IR35 decision wrong can be huge for the individual contractors as HMRC will demand penalties and interest on top of any underpaid tax. HMRC can look back many years to correct the tax position and defending your decision in court can be costly in terms of money, time and emotional strain.

However the tax savings from working through your own company can be significant. If the IR35 rules do not apply you can take most of the profits as dividends which are taxed at much lower rates than earnings and do not carry employers’ or employees’ NIC.

We can help you understand whether IR35 applies to your contracts but it is essential that the written contract accurately reflects your working relationship with your engager.

Companies spared tax rise

Last year the Chancellor Rishi Sunak proposed increasing corporation tax rates such that companies with annual profits of over £250,000 would pay tax at 25%.

Those with annual profits of less than £50,000 would continue to pay tax at 19% but a marginal tax rate of around 26.5% would apply on profits between £50,000 and £250,000.

The new Chancellor Kwasi Kwarteng has decided to keep the main rate of corporation tax at 19% at all profit levels. This will certainly keep corporation tax calculations simple and benefit profitable companies with higher profits.

Companies can currently claim a super deduction of 130% of the cost of new equipment purchased before April 2023. This deduction is likely to be modified or scrapped as it was introduced to encourage companies to invest before the corporation tax rate increased to 25%.

Instead businesses will be encouraged to claim under the annual investment allowance (AIA) which gives 100% relief for the cost of any qualifying equipment whether it was purchased new or second hand. The AIA can cover purchases totalling up to £1m per year and this cap will now be kept at that level indefinitely.

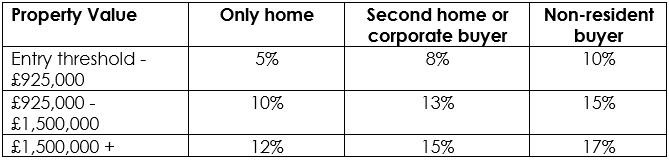

Home buyers to pay less stamp duty

When buying a residential property in England or Northern Ireland you have to pay stamp duty land tax (SDLT) if the purchase price exceeds a minimum threshold set at £125,000 since 2006.

In last week’s Budget the Chancellor announced that the entry threshold for SDLT payable on residential properties would double to £250,000 for deals completed on or after 23 September 2022.

Where none of the purchasers of the property has ever owned a property they can take advantage of a first-time buyer minimum SDLT threshold of £425,000 increased from £300,000. If the property costs more than £625,000 (previously £500,000) the first-time buyer threshold does not apply.

The rates of SDLT were not changed in the Budget other than to remove the lowest rate. Tax is due at the following rates:

When buying in Scotland or Wales you will pay the appropriate land taxes for those countries, which have different rates and thresholds.

Crack down on cloned companies

The National Crime Agency estimates that £78m was lost in cloned companies scams in 2020 and that is probably an underestimate as many frauds are not reported.

Criminals set up companies with names that are nearly identical to genuine trading or finance companies and then approach the customers of the genuine companies asking them to pay the fake company instead. With all transactions and communications online this form of fraud is easier to fall for.

The fraudsters will take great care to copy accurately the documentation and website of the real company so that instructions to pay to a different bank account appear genuine. If you are asked to make payments to a different bank account, always check by phoning your supplier on a number with which you are familiar.

The Government is finally tackling this issue by giving the Companies House Register more powers to challenge names of new companies. Any name which could be used to facilitate certain crimes will be rejected.

The register will also have powers to require existing companies to change their names if the name could be used for crime or suggests that the company is connected to an international institution or foreign government. Where the company fails to comply, the disputed name will be removed from the Companies House Register and replaced by the company number.

When dealing with a new supplier always check the Companies House Register (https://www.gov.uk/get-information-about-a-company) to see if the details of its registered address, directors and accounts are as you would expect.

Tax incentives in investment zones

The Government wants to designate up to 38 areas across England as investment zones which will benefit from special tax reliefs and relaxed planning laws.

The tax reliefs will include:

• employers’ Class 1 NIC at 0% on earnings of new employees employed in the zone for at least 60% of their working hours, capped at earnings of £50,270 per person (normal employers’ NIC will apply to earnings above that level);

• 100% first year capital allowance on the cost of equipment used in the zone;

• no SDLT payable on the acquisition of commercial buildings bought for use or development in the zone;

• no SDLT on land or buildings acquired to build or convert into new homes in the zone; and

• 100% relief from business rates on newly occupied buildings.

The local authorities for the proposed investment zones need to give consent before the zone is activated and in return they will receive all of the additional business rates collected from within the zone. However some control over planning decisions within the zone will be lost.

Areas in Scotland, Wales and Northern Ireland could also be designated as investment zones if the devolved administrations for those areas agree.

NIC cut in November

The Government has decided to reverse the 1.25 percentage point increases in national insurance contribution (NIC) rates which were introduced from 6 April 2022.

The rates of Class 1 NIC are taken back to the levels that were in place on 5 April 2022 but only with effect for pay periods beginning on and after 6 November 2022. The NIC thresholds which were increased from 6 July 2022 are not being reversed. The new rates will be:

Employees’ Class 1 NIC

• 12% (was 13.25%) on earnings in the band: £1,048 to £4,189 per month (£12,570 to £50,270 per year)

• 2% (was 3.25%) on earnings above £4,189 per month (£50,270 per year)

Employers’ Class 1 NIC

• 13.8% (was 15.05%) on earnings above £758 per month (£9,100 per year).

This will be the third change in NIC rates or thresholds in this tax year but the Government is confident that software developers will be able to amend their payroll programs in time for the November payroll run.

Where NIC is calculated over the full tax year, for example on benefits or for a director who has an annual pay period, the rates for the year are blended. Directors will pay Class 1 NIC at 12.73% on earnings between £11,908 and £50,270 with 2.73% applying to earnings over £50,270. The director’s employer will pay Class 1 NIC at 14.53%.

The self-employed pay Class 4 NIC, calculated as a percentage of their annual profits, with the final payment of income tax due for the year. The new rates of Class 4 NIC for 2022-23 will be:

• 9.73% on profits between £12,570 and £50,270

• 2.73% on profits above £50,270.

Some people may benefit from changing their planned remuneration strategies, especially in relation to timing of payments. We can help you determine the most efficient way for you to be paid or extract profits.

Get in Touch

Please contact us if you need further advice, have any questions about our services, or would like a free consultation or a fixed quote.